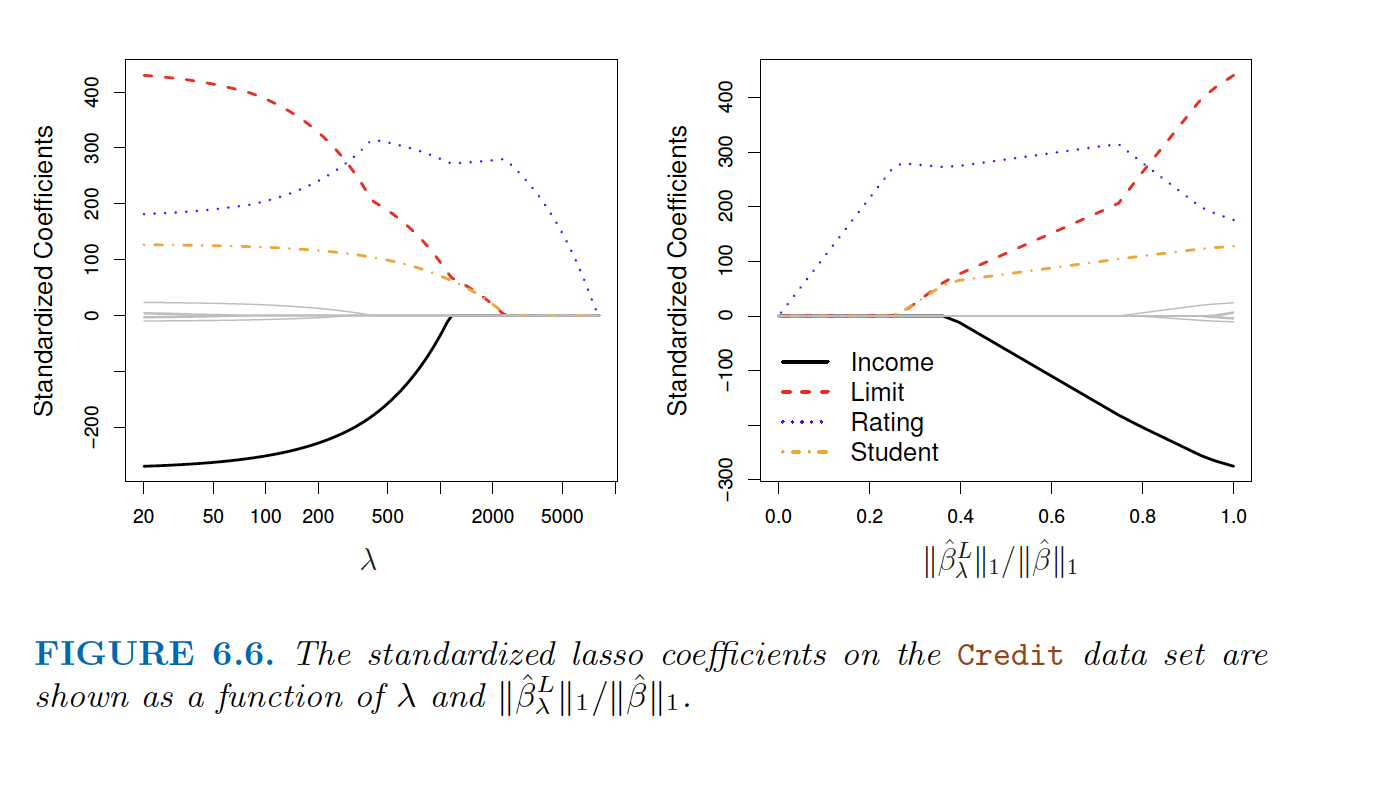

The Lasso

- \(\hat{\beta}^L \equiv \underset{\hat{\beta}}{argmin}(RSS + \lambda\sum_{k=1}^p{|\beta_k|})\)

- Shrinks some coefficients to 0 (creates sparse models)

How lasso eliminiates predictors.

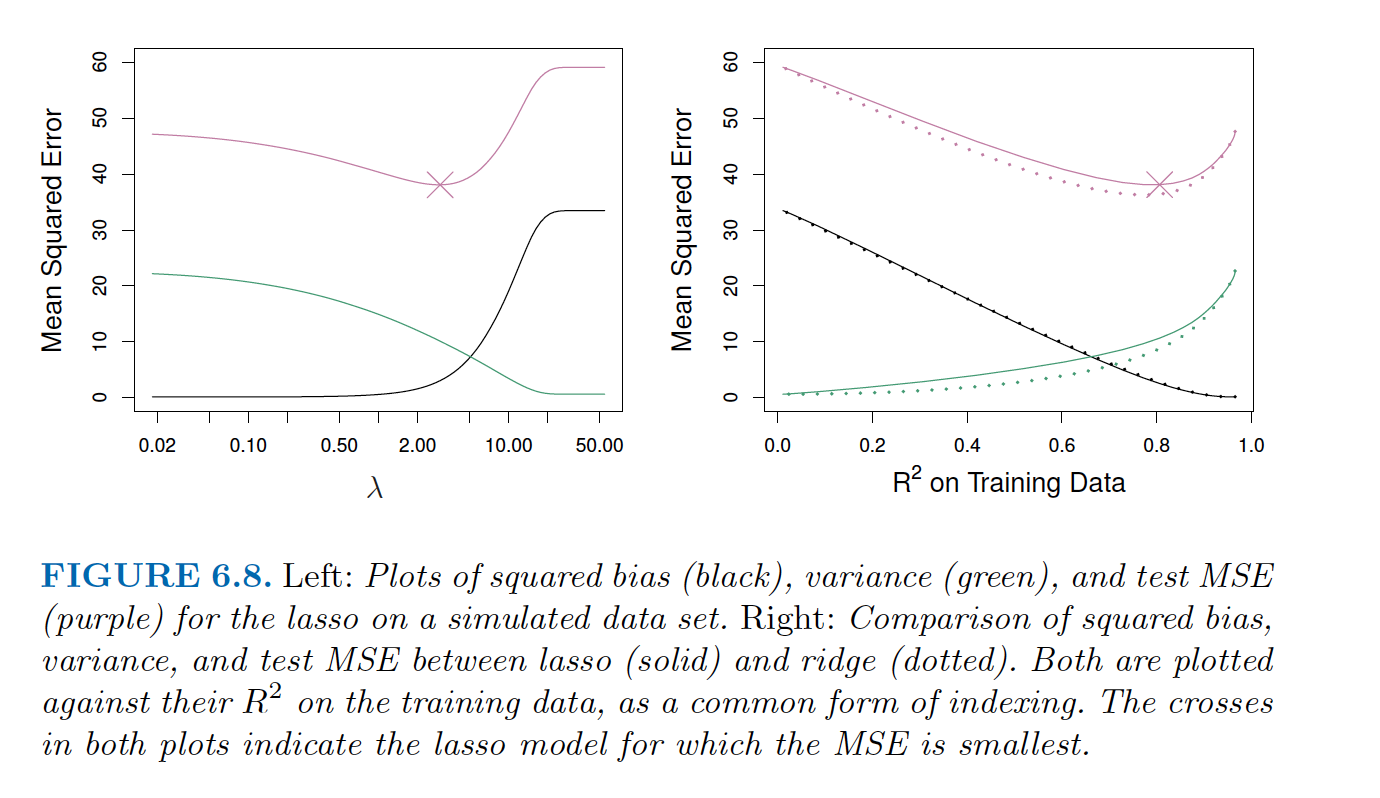

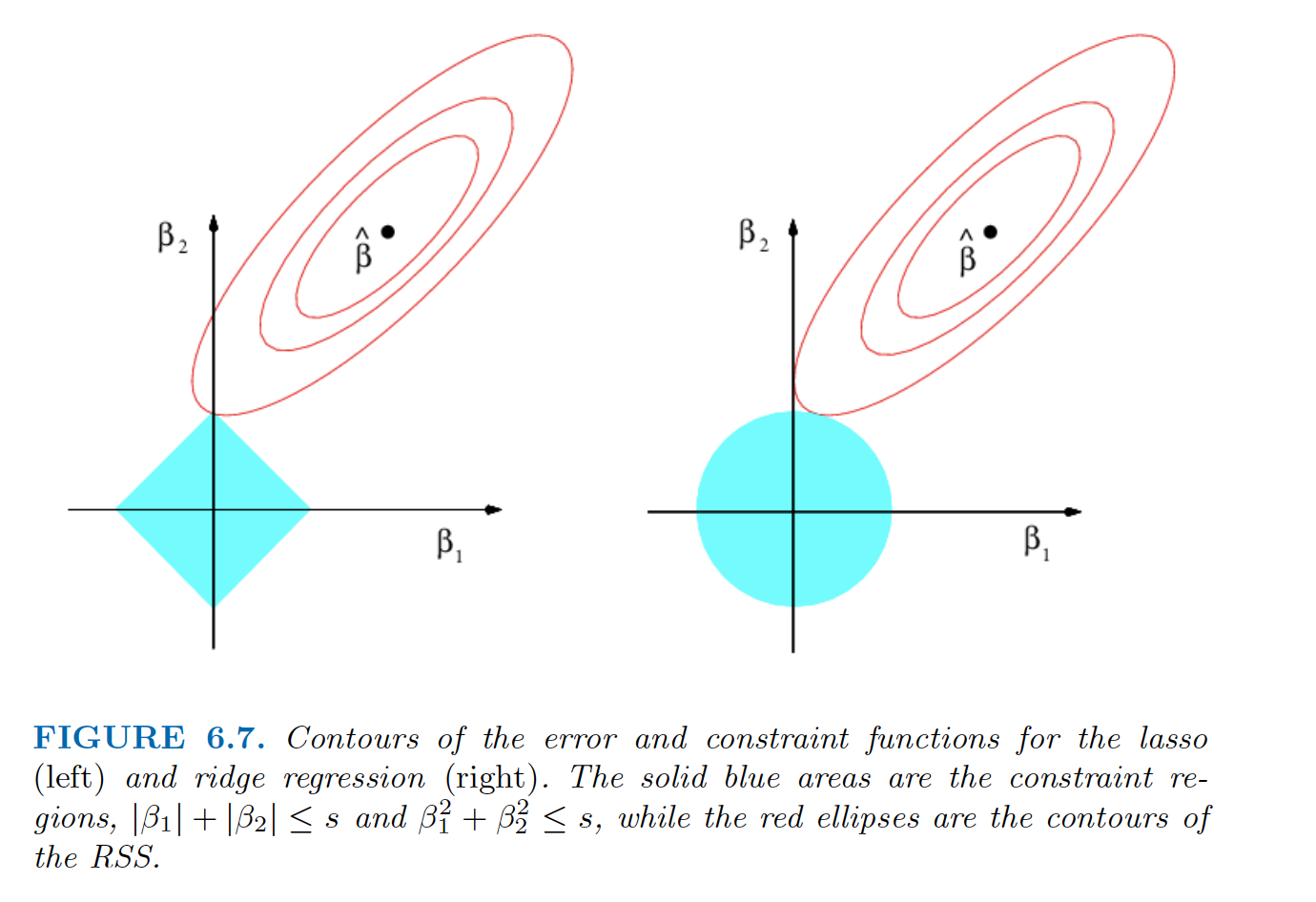

It can be shown that these shrinkage methods are equivalent to a OLS with a constraint that depends on the type of shrinkage. For two parameters:

\(|\beta_1|+|\beta_2| \leq s\) for lasso,

\(\beta_1^2+\beta_2^2 \leq s\) for ridge,

The value of s depends on \(\lambda\). (Larger s corresponds to smaller \(\lambda\)).

Graphically:

“the lasso constraint has corners at each of the axes, and so the ellipse will often intersect the constraint region at an axis”