Ridge Regression

Ridge regression is very similar to least squares, except that the coefcients are estimated by minimizing a slightly diferent quantity

\(\hat{\beta}^{OLS} \equiv \underset{\hat{\beta}}{argmin}(RSS)\)

\(\hat{\beta}^R \equiv \underset{\hat{\beta}}{argmin}(RSS+\lambda\sum_{k=1}^p{\beta_k^2})\)

\(\lambda\) tuning parameter (hyperparameter) for the shrinkage penalty

there’s one model parameter \(\lambda\) doesn’t shrink

- (\(\hat{\beta_0}\))

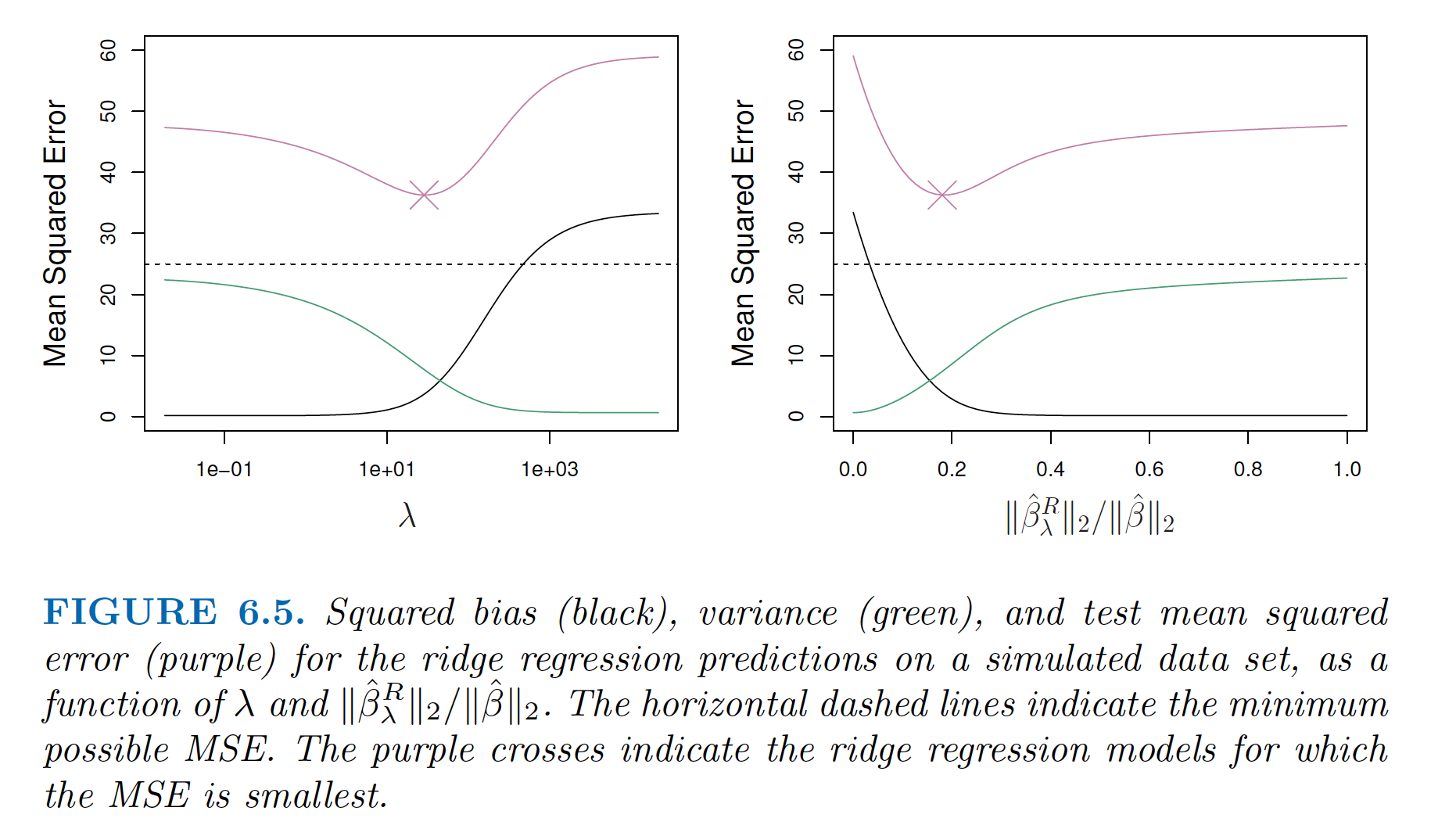

Ridge Regression, Visually

\[\|\beta\|_2 = \sqrt{\sum_{j=1}^p{\beta_j^2}}\]

Note the decrease in test MSE, and further that this is not computationally expensive: “One can show that computations required to solve (6.5), simultaneously for all values of \(\lambda\), are almost identical to those for fitting a model using least squares.”