3.2 Time series components

Time series are made of three components:

- a trend-cycle component \(T_t\)

- a seasonal component \(S_t\)

- a remainder component \(R_t\)

3.2.1 Additive decomposition

When the variation around the trend-cycle does not vary with the level of the time series.

\[y_t=S_t+T_t+R_t\]

3.2.2 Multiplicative decomposition

When the variation in the seasonal pattern, or the variation around the trend-cycle, appears to be proportional to the level of the time series.

\[y_t=S_t*T_t*R_t\] An alternative can be a log transformation

\[log(y_t)=log(S_t)+log(T_t)+log(R_t)\]

3.2.3 Example: Employment in the US retail sector

A nice introduction to the use of the {fpp3} package by the author is in the section Example at minute 13.11 here: Dr. Rob J. Hyndman - Ensemble Forecasts with {fable}

Data

## # A tsibble: 6 x 4 [1M]

## # Key: Series_ID [1]

## Month Series_ID Title Employed

## <mth> <chr> <chr> <dbl>

## 1 1939 Jan CEU0500000001 Total Private 25338

## 2 1939 Feb CEU0500000001 Total Private 25447

## 3 1939 Mar CEU0500000001 Total Private 25833

## 4 1939 Apr CEU0500000001 Total Private 25801

## 5 1939 May CEU0500000001 Total Private 26113

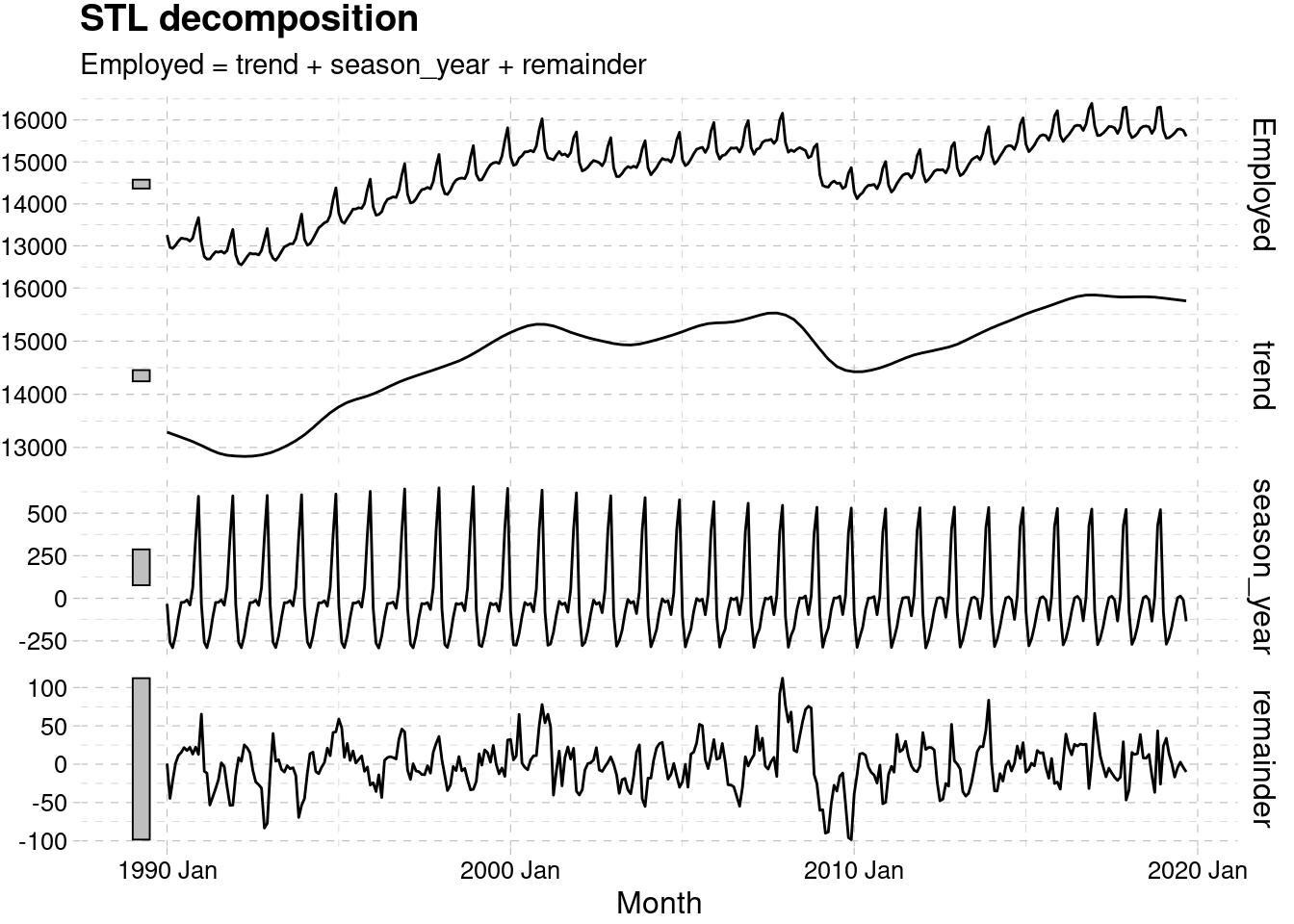

## 6 1939 Jun CEU0500000001 Total Private 264853.2.3.1 STL decomposition method

Seasonal and Trend decomposition using Loess.

Some interesting information about the STL model:

- it is additive

- it is iterative and relies on the alternate estimation of the trend

- the seasonal components are locally estimated scatterplot smoothing (Loess)

- it estimates nonlinear relationships

- the seasonal component is allowed to change over time

- it is composed of seasonal patterns estimated based on k consecutive seasonal cycles

- k controls how rapidly the seasonal component can change

- it is robust to outliers and missing data

- it is able to decompose time series with seasonality of any frequency, and provides implementation using numerical methods instead of mathematical modeling.

More info here: R. B. Cleveland et al. (1990)

The command used is:

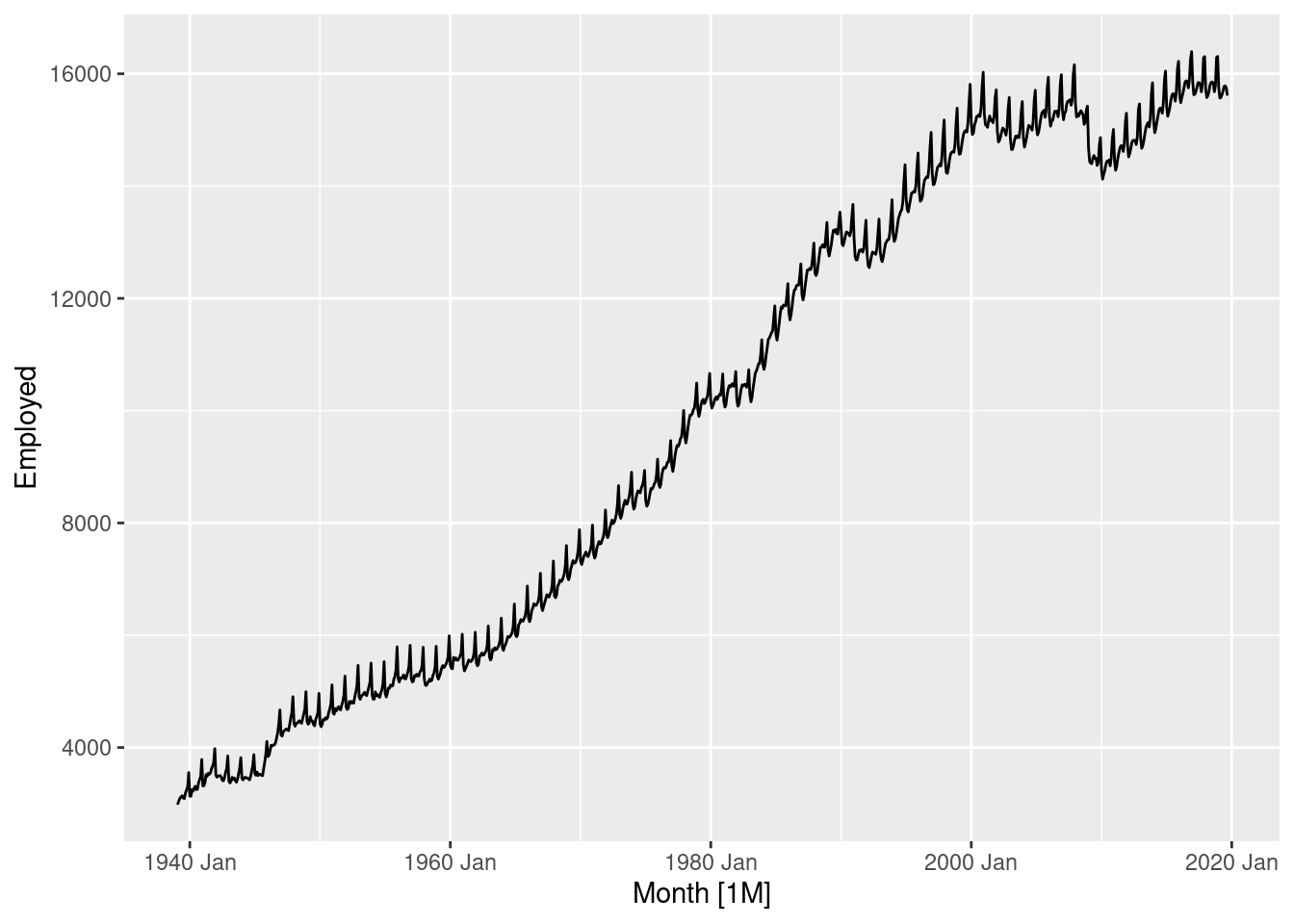

model(stl = STL(<formula>))us_employment%>% #year(Month) >= 1990,

filter(Title == "Retail Trade") %>%

select(-Series_ID) %>%

autoplot()## Plot variable not specified, automatically selected `.vars = Employed`

us_retail_employment <- us_employment %>%

filter(year(Month) >= 1990, Title == "Retail Trade") %>%

select(-Series_ID)

dcmp <- us_retail_employment %>%

model(stl = STL(Employed))

components(dcmp) %>%

autoplot()+

ggthemes::theme_pander()

?components

methods("components")## # A tsibble: 6 x 5 [1M]

## Month Employed trend season_adjust remainder

## <mth> <dbl> <dbl> <dbl> <dbl>

## 1 1990 Jan 13256. 13288. 13289. 0.836

## 2 1990 Feb 12966. 13269. 13224. -44.6

## 3 1990 Mar 12938. 13250. 13228. -22.1

## 4 1990 Apr 13012. 13231. 13232. 1.05

## 5 1990 May 13108. 13211. 13223. 11.3

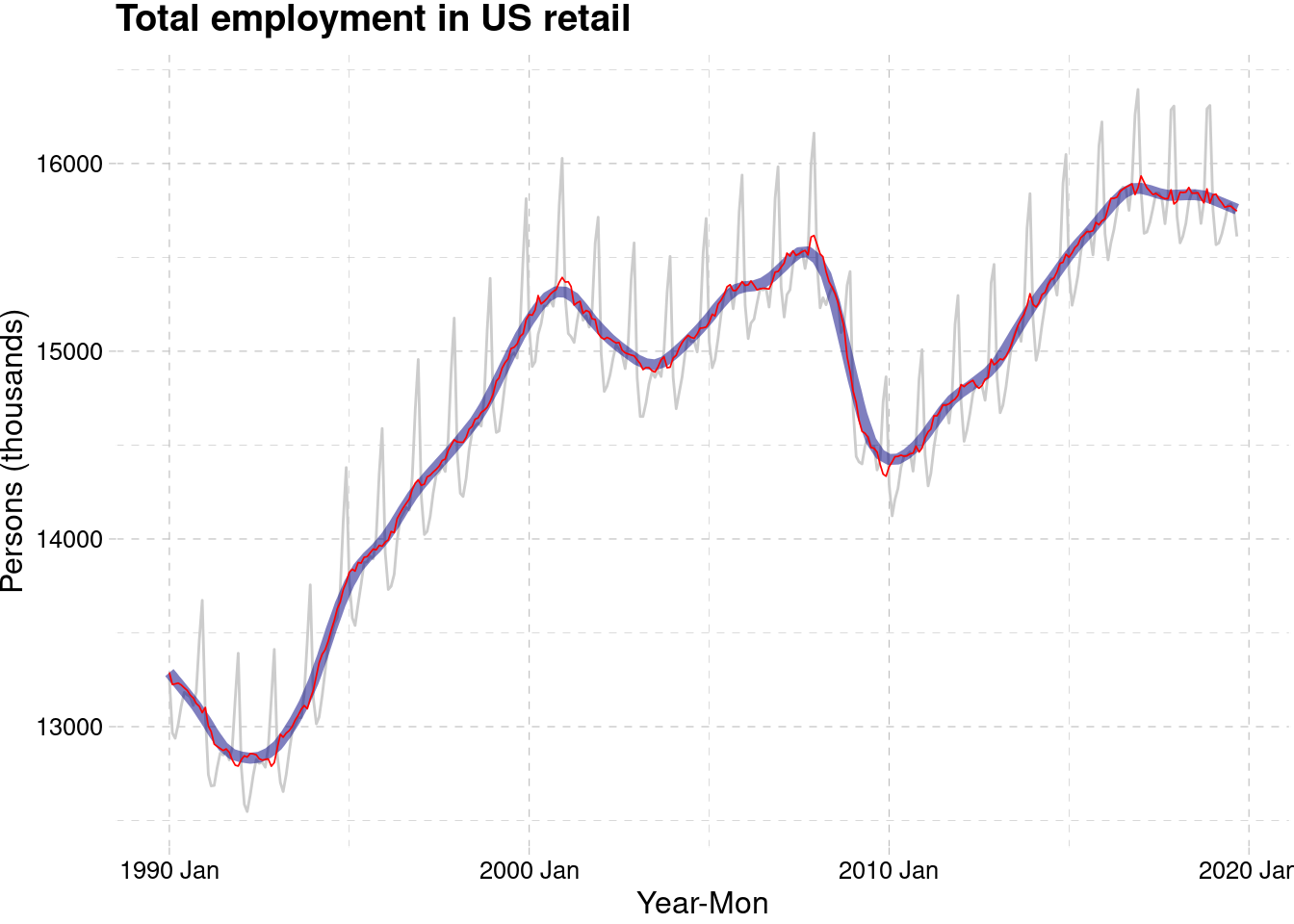

## 6 1990 Jun 13183. 13192. 13207. 15.5components(dcmp) %>%

as_tsibble() %>%

autoplot(Employed, colour="grey80") +

geom_line(aes(y=trend), colour = "navy",linewidth=2,alpha=0.5) +

geom_line(aes(y=season_adjust), colour = "red",linewidth=0.3) +

# geom_line(aes(y=remainder), colour = "blue") +

labs(y = "Persons (thousands)",x="Year-Mon",

title = "Total employment in US retail")+

ggthemes::theme_pander()