12.1 Complex seasonality

Daily data:

- weekly pattern (365.25/7 \(\approx\) 52.179 on average)

- annual pattern

Hourly data:

- daily pattern

- weekly pattern

- annual pattern

12.1.1 Case Study 1

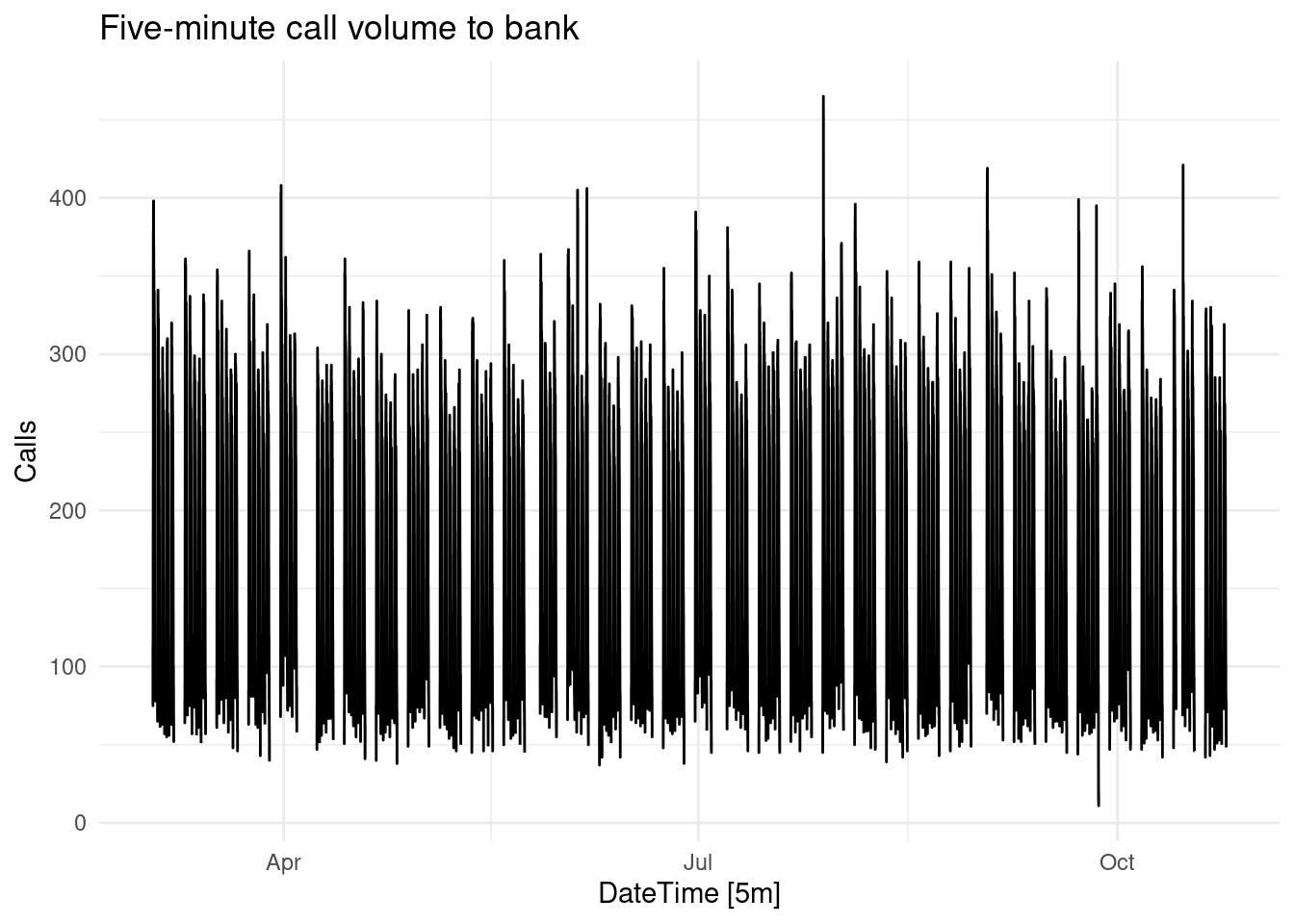

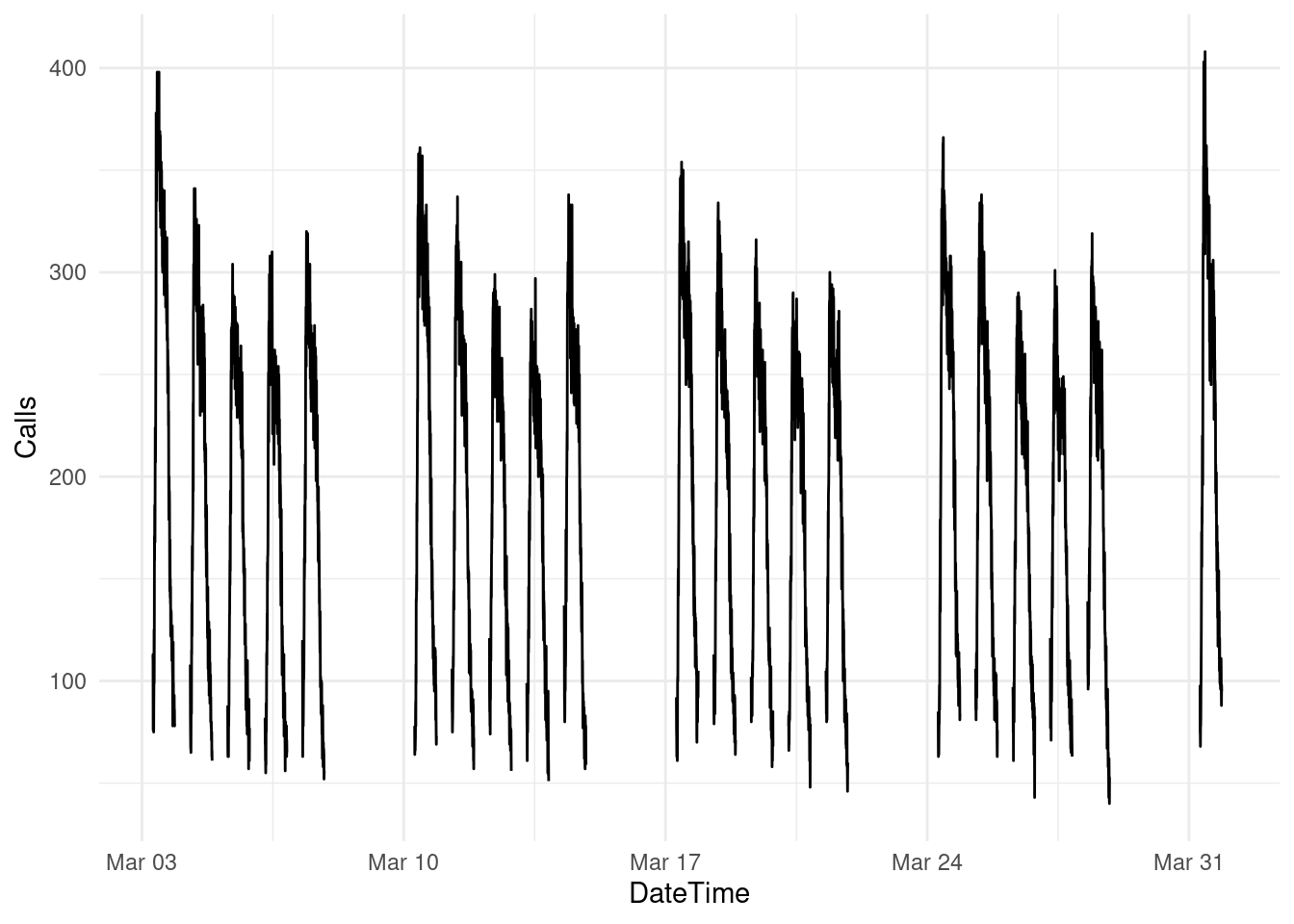

Number of calls (call volume) to a North American commercial bank per 5-minute interval between 7:00am and 9:05pm each weekday over a 33 week period.

In this case we have a weak daily and weekly seasonal patterns:

- on a total of

164 daysfrom March 03, 2003 to Oct 24, 2003. - there are

169 5-minute intervals per day: \[169×5=845\] - a total of

845 minutes per day(5-days a week) spent on bank calls.

Let’s have a look at the seasonality per day and per week.

## # A tsibble: 6 x 2 [5m] <UTC>

## DateTime Calls

## <dttm> <dbl>

## 1 2003-03-03 07:00:00 111

## 2 2003-03-03 07:05:00 113

## 3 2003-03-03 07:10:00 76

## 4 2003-03-03 07:15:00 82

## 5 2003-03-03 07:20:00 91

## 6 2003-03-03 07:25:00 87## # A tsibble: 6 x 2 [5m] <UTC>

## DateTime Calls

## <dttm> <dbl>

## 1 2003-10-24 20:35:00 56

## 2 2003-10-24 20:40:00 64

## 3 2003-10-24 20:45:00 49

## 4 2003-10-24 20:50:00 54

## 5 2003-10-24 20:55:00 55

## 6 2003-10-24 21:00:00 54## # A tibble: 6 × 2

## date n

## <date> <int>

## 1 2003-03-03 169

## 2 2003-03-04 169

## 3 2003-03-05 169

## 4 2003-03-06 169

## 5 2003-03-07 169

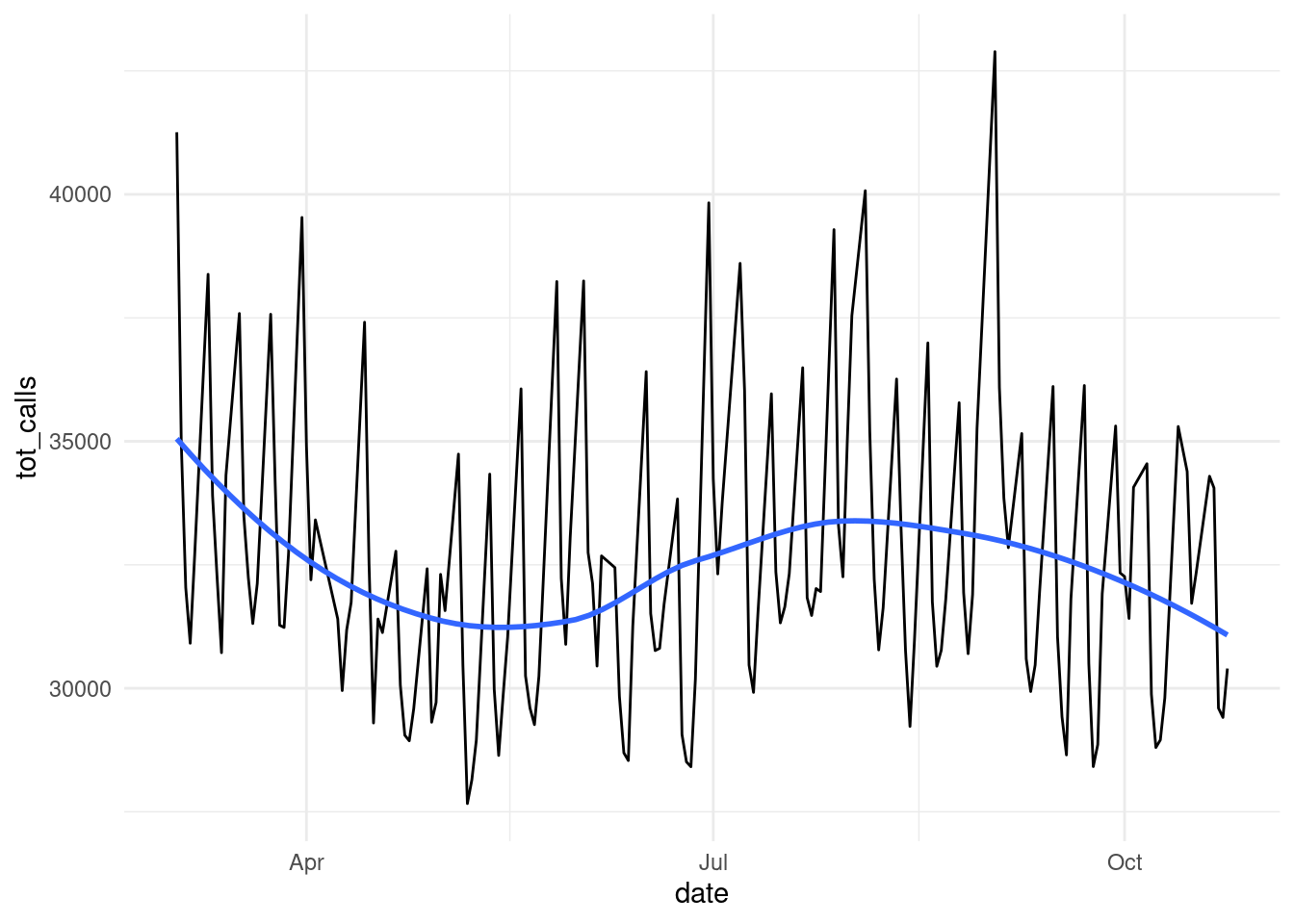

## 6 2003-03-10 169per_day <- bank_calls%>%

mutate(date=as.Date(DateTime))%>%

group_by(date)%>%

reframe(tot_calls=sum(Calls))

per_day%>%dim## [1] 164 2We cannot see a clear pattern for seasonality here.

## `geom_smooth()` using method = 'loess' and formula = 'y ~ x'

bank_calls |>

fill_gaps() |>

autoplot(Calls) +

labs(y = "Calls",

title = "Five-minute call volume to bank")

bank_calls |>

fill_gaps() %>%

mutate(month=month(DateTime),

day=day(DateTime),

week=week(DateTime))%>%

filter(month<4)%>%

ggplot(aes(x=DateTime,y=Calls,group=week))+

geom_line()## Warning: Removed 511 rows containing missing values or values outside the scale range

## (`geom_line()`).

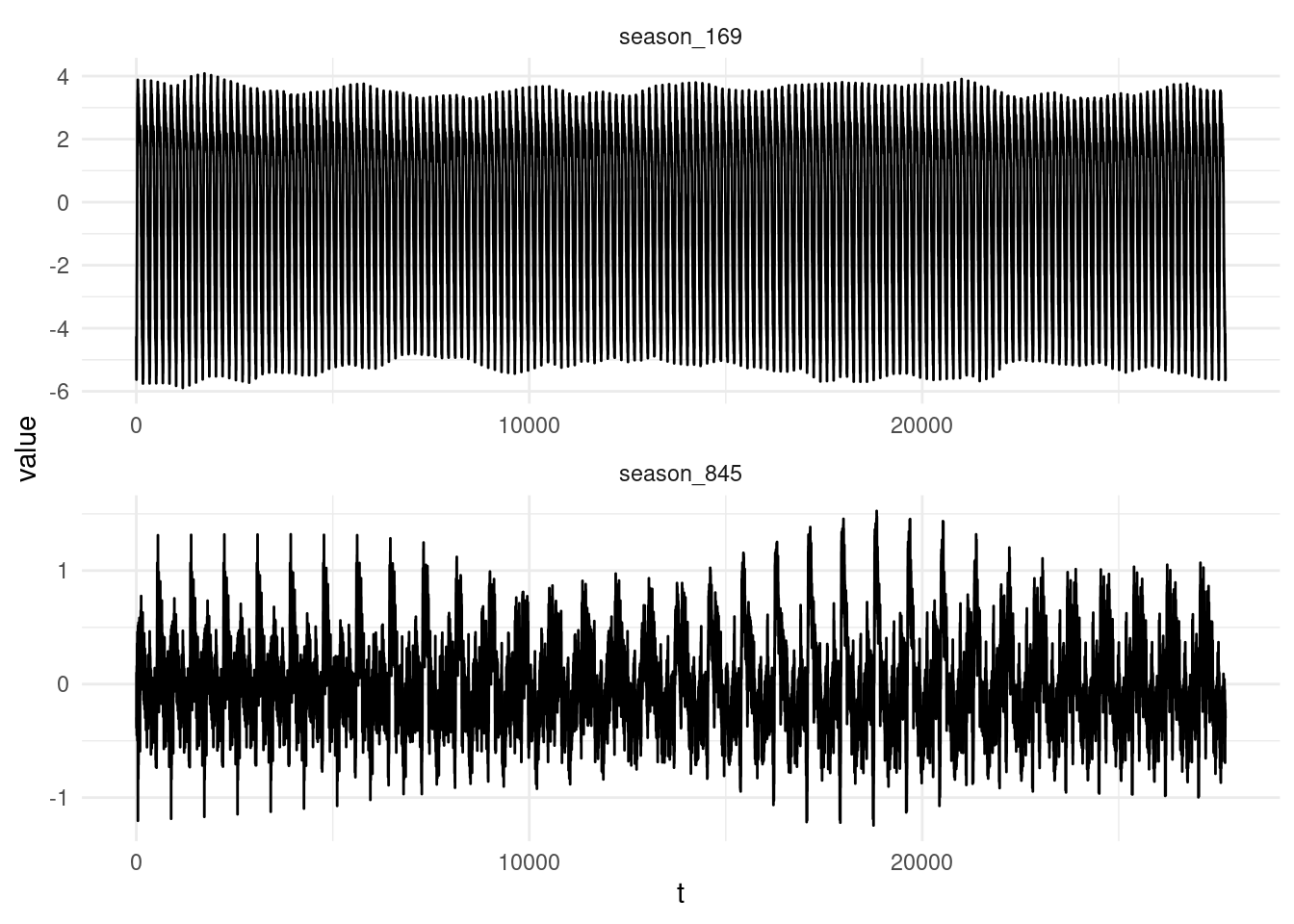

Have a look at multiple seasonality with the STL() decomposition:

calls <- bank_calls |>

mutate(t = row_number()) |>

update_tsibble(index = t, regular = TRUE)

calls%>%head## # A tsibble: 6 x 3 [1]

## DateTime Calls t

## <dttm> <dbl> <int>

## 1 2003-03-03 07:00:00 111 1

## 2 2003-03-03 07:05:00 113 2

## 3 2003-03-03 07:10:00 76 3

## 4 2003-03-03 07:15:00 82 4

## 5 2003-03-03 07:20:00 91 5

## 6 2003-03-03 07:25:00 87 6calls |>

model(

STL(sqrt(Calls) ~ season(period = 169) +

season(period = 5*169),

robust = TRUE)

) |>

components() |>

select(t,season_169,season_845) %>%

pivot_longer(cols = c("season_169","season_845"))%>%

ggplot(aes(x=t,y=value)) +

geom_line()+

facet_wrap(vars(name),ncol = 1,scales = "free")

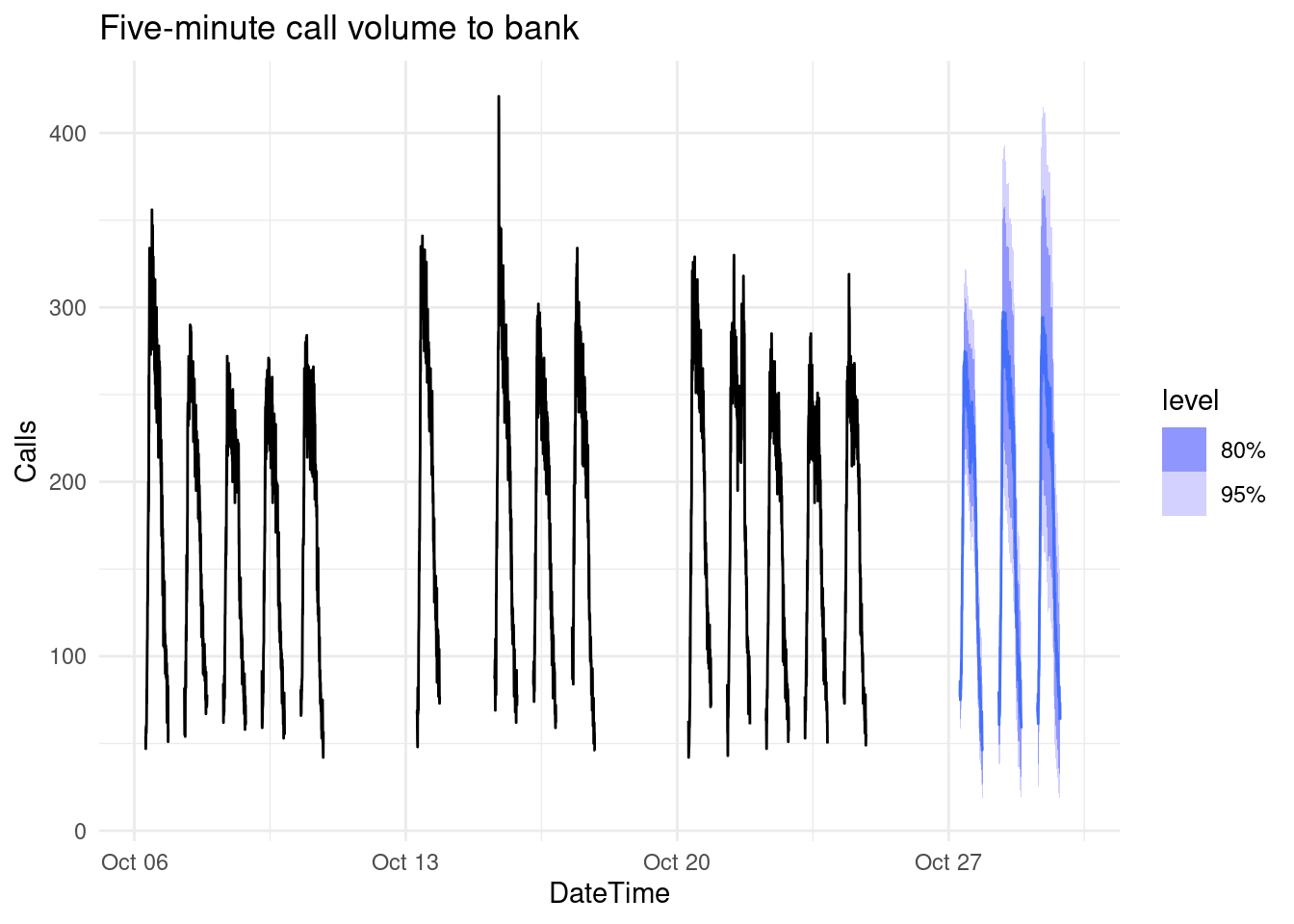

Decomposition used in forecasting:

# Forecasts from STL+ETS decomposition

my_dcmp_spec <- decomposition_model(

STL(sqrt(Calls) ~ season(period = 169) +

season(period = 5*169),

robust = TRUE),

# ETS decomposition

ETS(season_adjust ~ season("N"))

)Forecast 5*169 forward

## # A fable: 6 x 4 [1]

## # Key: .model [1]

## .model t Calls .mean

## <chr> <dbl> <dist> <dbl>

## 1 my_dcmp_spec 27717 t(N(8.8, 0.24)) 76.8

## 2 my_dcmp_spec 27718 t(N(9.2, 0.25)) 85.7

## 3 my_dcmp_spec 27719 t(N(8.9, 0.25)) 79.8

## 4 my_dcmp_spec 27720 t(N(8.6, 0.26)) 75.0

## 5 my_dcmp_spec 27721 t(N(9.2, 0.27)) 85.0

## 6 my_dcmp_spec 27722 t(N(8.7, 0.28)) 75.7# Add correct time stamps to fable

fc_with_times <- bank_calls |>

new_data(n = 7 * 24 * 60 / 5) |>

mutate(time = format(DateTime, format = "%H:%M:%S")) |>

filter(

time %in% format(bank_calls$DateTime, format = "%H:%M:%S"),

wday(DateTime, week_start = 1) <= 5

) |>

mutate(t = row_number() + max(calls$t)) |>

left_join(fc, by = "t") |>

as_fable(response = "Calls", distribution = Calls)

fc_with_times%>%head()## # A fable: 6 x 6 [5m] <UTC>

## DateTime time t .model Calls .mean

## <dttm> <chr> <dbl> <chr> <dist> <dbl>

## 1 2003-10-27 07:00:00 07:00:00 27717 my_dcmp_spec t(N(8.8, 0.24)) 76.8

## 2 2003-10-27 07:05:00 07:05:00 27718 my_dcmp_spec t(N(9.2, 0.25)) 85.7

## 3 2003-10-27 07:10:00 07:10:00 27719 my_dcmp_spec t(N(8.9, 0.25)) 79.8

## 4 2003-10-27 07:15:00 07:15:00 27720 my_dcmp_spec t(N(8.6, 0.26)) 75.0

## 5 2003-10-27 07:20:00 07:20:00 27721 my_dcmp_spec t(N(9.2, 0.27)) 85.0

## 6 2003-10-27 07:25:00 07:25:00 27722 my_dcmp_spec t(N(8.7, 0.28)) 75.7# Plot results with last 3 weeks of data

fc_with_times |>

fill_gaps() |>

autoplot(bank_calls |> tail(14 * 169) |> fill_gaps()) +

labs(y = "Calls",

title = "Five-minute call volume to bank")## Warning: Removed 100 rows containing missing values or values outside the scale range

## (`geom_line()`).

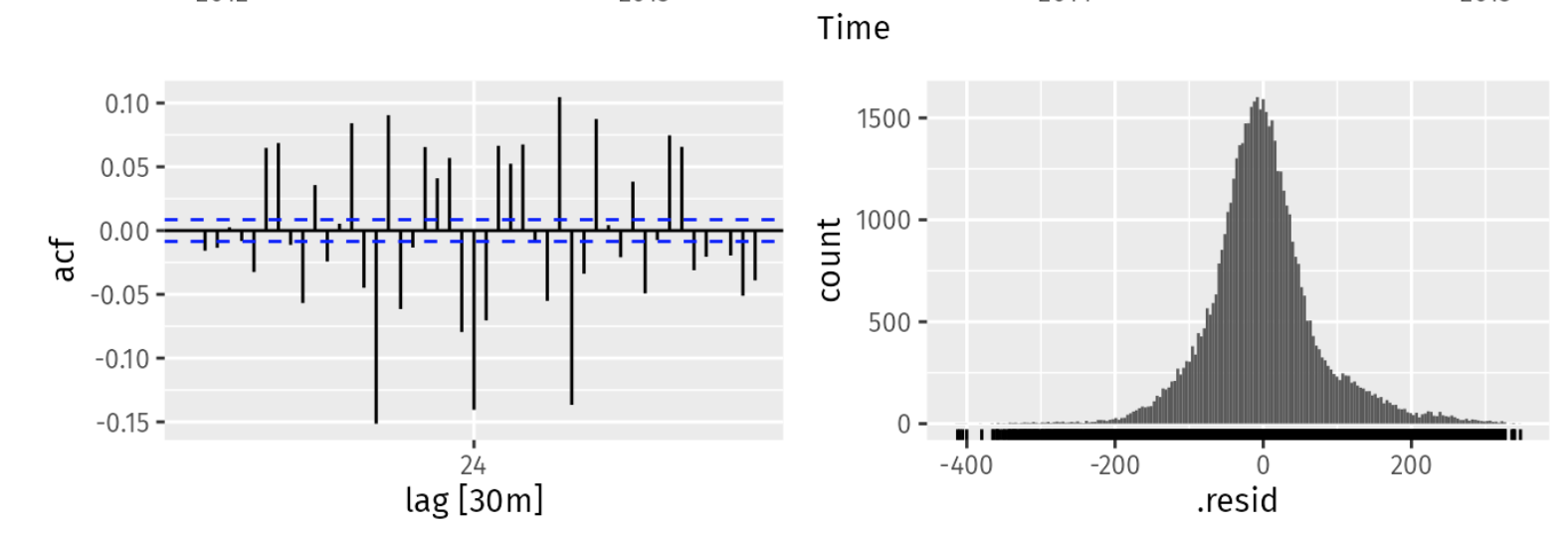

Apply Fourier for multiple seasonalities: fit a dynamic harmonic regression model with an ARIMA error structure.

fit <- calls |>

model(

dhr = ARIMA(sqrt(Calls) ~ PDQ(0, 0, 0) + pdq(d = 0) +

fourier(period = 169, K = 10) +

fourier(period = 5*169, K = 5)))# Add correct time stamps to fable

fc_with_times <- bank_calls |>

new_data(n = 7 * 24 * 60 / 5) |>

mutate(time = format(DateTime,

format = "%H:%M:%S")) |>

filter(

time %in% format(bank_calls$DateTime,

format = "%H:%M:%S"),

wday(DateTime, week_start = 1) <= 5

) |>

mutate(t = row_number() + max(calls$t)) |>

left_join(fc, by = "t") |>

as_fable(response = "Calls", distribution = Calls)12.1.2 Case Study 2

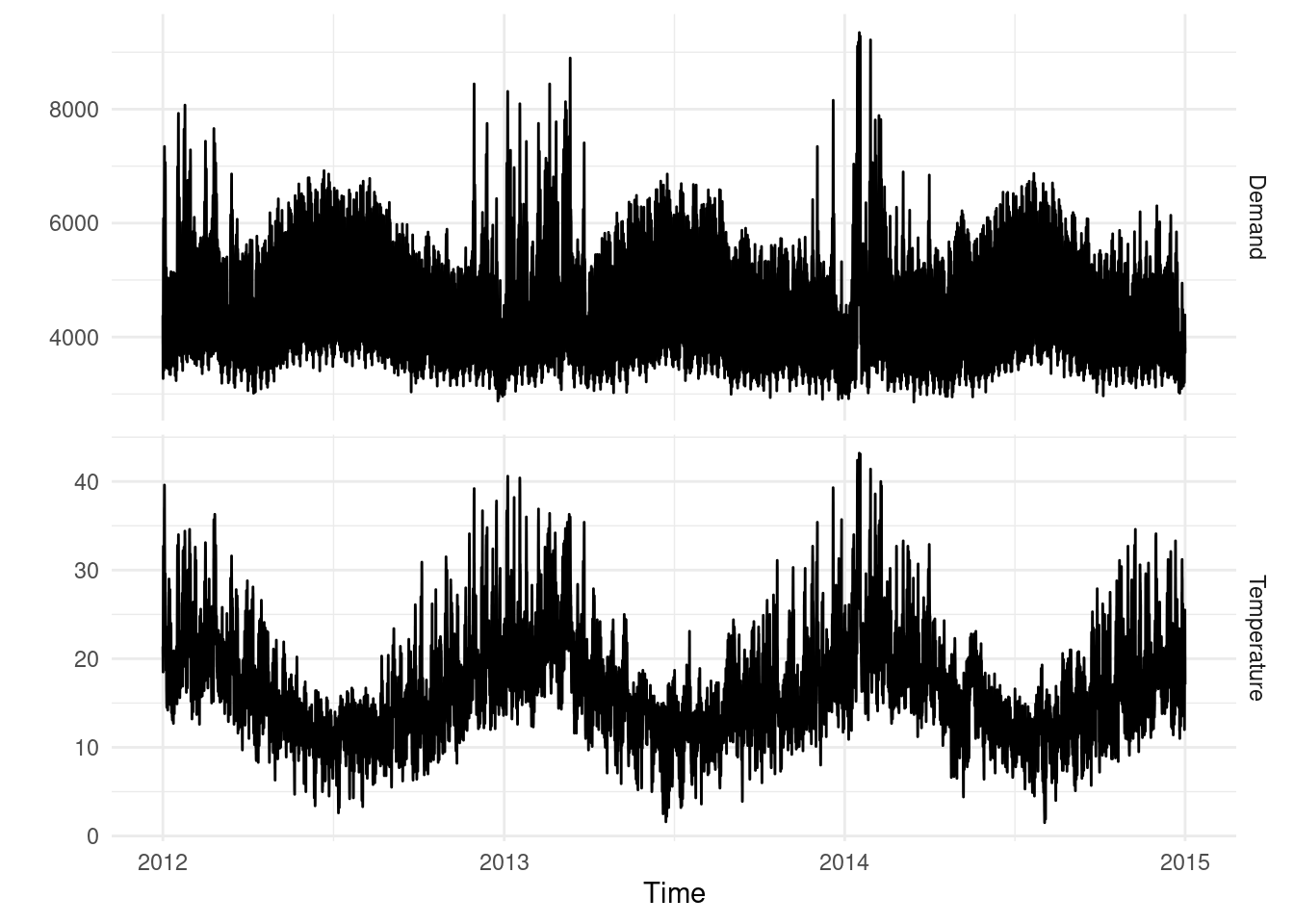

Electricity demand (MWh) in Victoria, Australia, during 2012–2014 (half-hourly) along with temperatures (degrees Celsius) for the same period for Melbourne.

## # A tsibble: 6 x 5 [30m] <Australia/Melbourne>

## Time Demand Temperature Date Holiday

## <dttm> <dbl> <dbl> <date> <lgl>

## 1 2012-01-01 00:00:00 4383. 21.4 2012-01-01 TRUE

## 2 2012-01-01 00:30:00 4263. 21.0 2012-01-01 TRUE

## 3 2012-01-01 01:00:00 4049. 20.7 2012-01-01 TRUE

## 4 2012-01-01 01:30:00 3878. 20.6 2012-01-01 TRUE

## 5 2012-01-01 02:00:00 4036. 20.4 2012-01-01 TRUE

## 6 2012-01-01 02:30:00 3866. 20.2 2012-01-01 TRUEvic_elec |>

pivot_longer(Demand:Temperature, names_to = "Series") |>

ggplot(aes(x = Time, y = value)) +

geom_line() +

facet_grid(rows = vars(Series), scales = "free_y") +

labs(y = "")

elec <- vic_elec |>

mutate(

DOW = wday(Date, label = TRUE),

Working_Day = !Holiday & !(DOW %in% c("Sat", "Sun")),

Cooling = pmax(Temperature, 18)

)

elec%>%head## # A tsibble: 6 x 8 [30m] <Australia/Melbourne>

## Time Demand Temperature Date Holiday DOW Working_Day

## <dttm> <dbl> <dbl> <date> <lgl> <ord> <lgl>

## 1 2012-01-01 00:00:00 4383. 21.4 2012-01-01 TRUE Sun FALSE

## 2 2012-01-01 00:30:00 4263. 21.0 2012-01-01 TRUE Sun FALSE

## 3 2012-01-01 01:00:00 4049. 20.7 2012-01-01 TRUE Sun FALSE

## 4 2012-01-01 01:30:00 3878. 20.6 2012-01-01 TRUE Sun FALSE

## 5 2012-01-01 02:00:00 4036. 20.4 2012-01-01 TRUE Sun FALSE

## 6 2012-01-01 02:30:00 3866. 20.2 2012-01-01 TRUE Sun FALSE

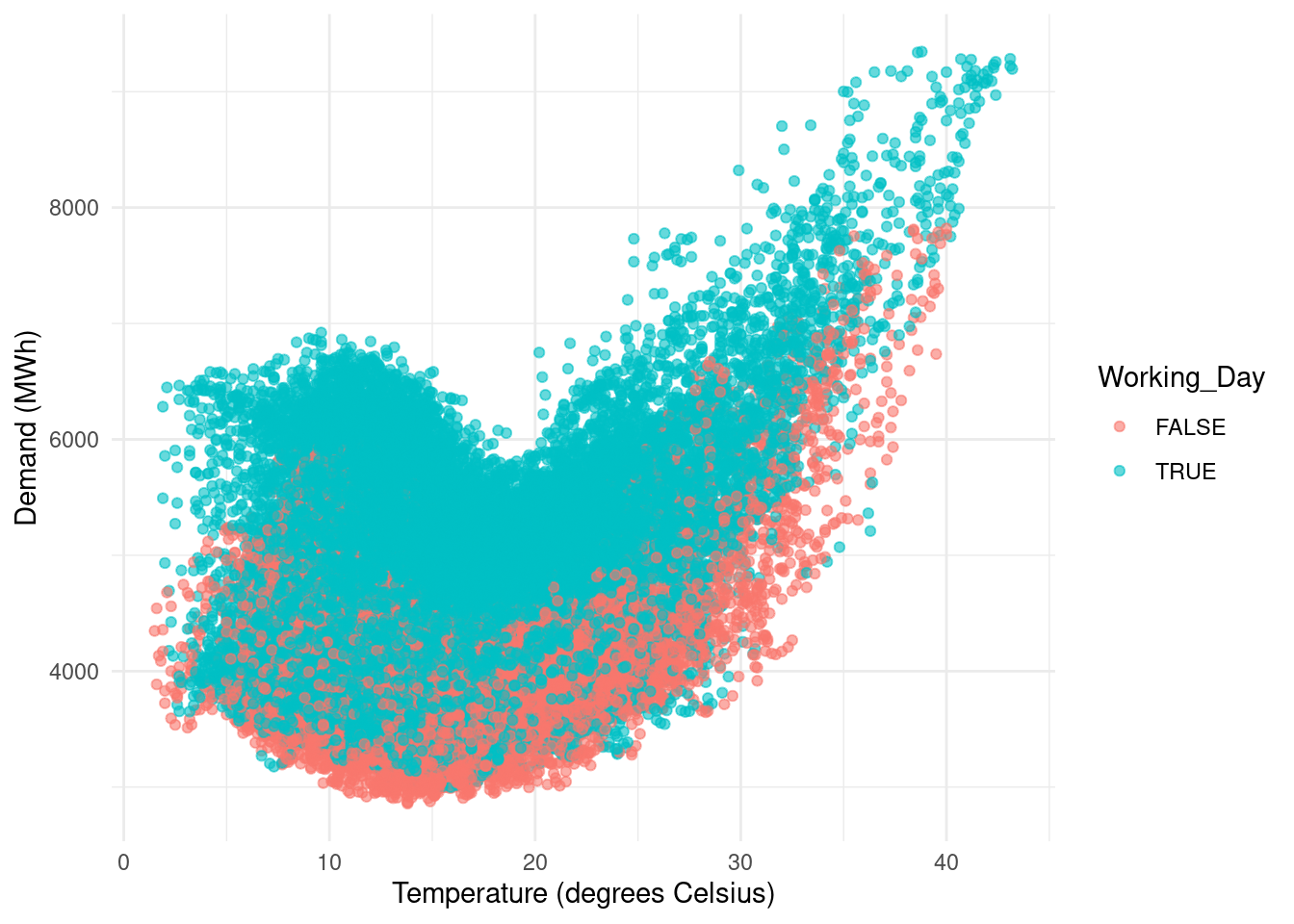

## # ℹ 1 more variable: Cooling <dbl>elec |>

ggplot(aes(x=Temperature, y=Demand, col=Working_Day)) +

geom_point(alpha = 0.6) +

labs(x="Temperature (degrees Celsius)", y="Demand (MWh)")

fit2 <- elec |>

model(

ARIMA(Demand ~ PDQ(0, 0, 0) + pdq(d = 0) +

Temperature + Cooling + Working_Day +

fourier(period = "day", K = 10) +

fourier(period = "week", K = 5) +

fourier(period = "year", K = 3))

)new_data:

elec_newdata <- new_data(elec, 2*48) |>

mutate(

Temperature = tail(elec$Temperature, 2 * 48),

Date = lubridate::as_date(Time),

DOW = wday(Date, label = TRUE),

Working_Day = (Date != "2015-01-01") &

!(DOW %in% c("Sat", "Sun")),

Cooling = pmax(Temperature, 18)

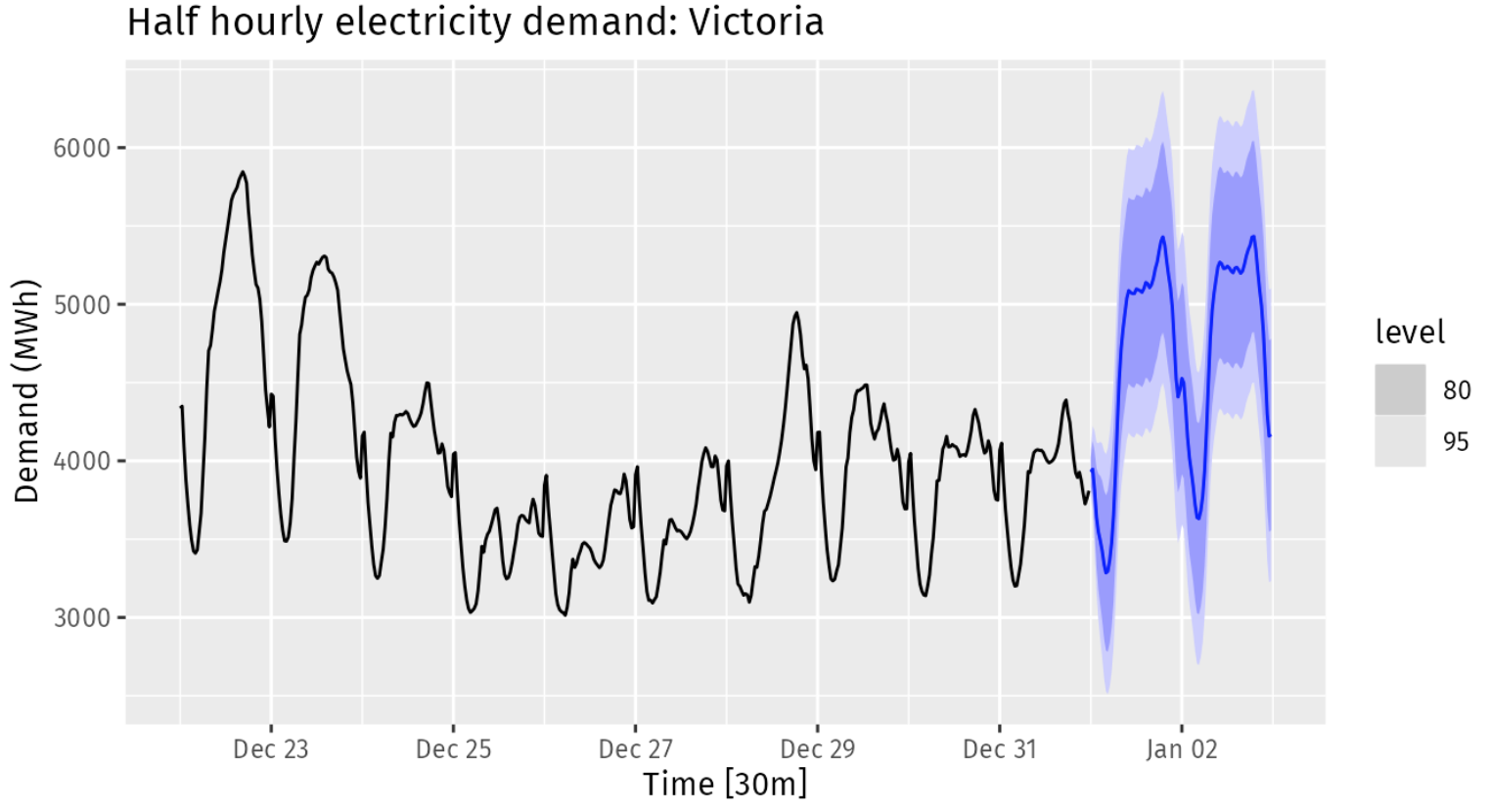

)fc |>

autoplot(elec |> tail(10 * 48)) +

labs(title="Half hourly electricity demand: Victoria",

y = "Demand (MWh)", x = "Time [30m]")