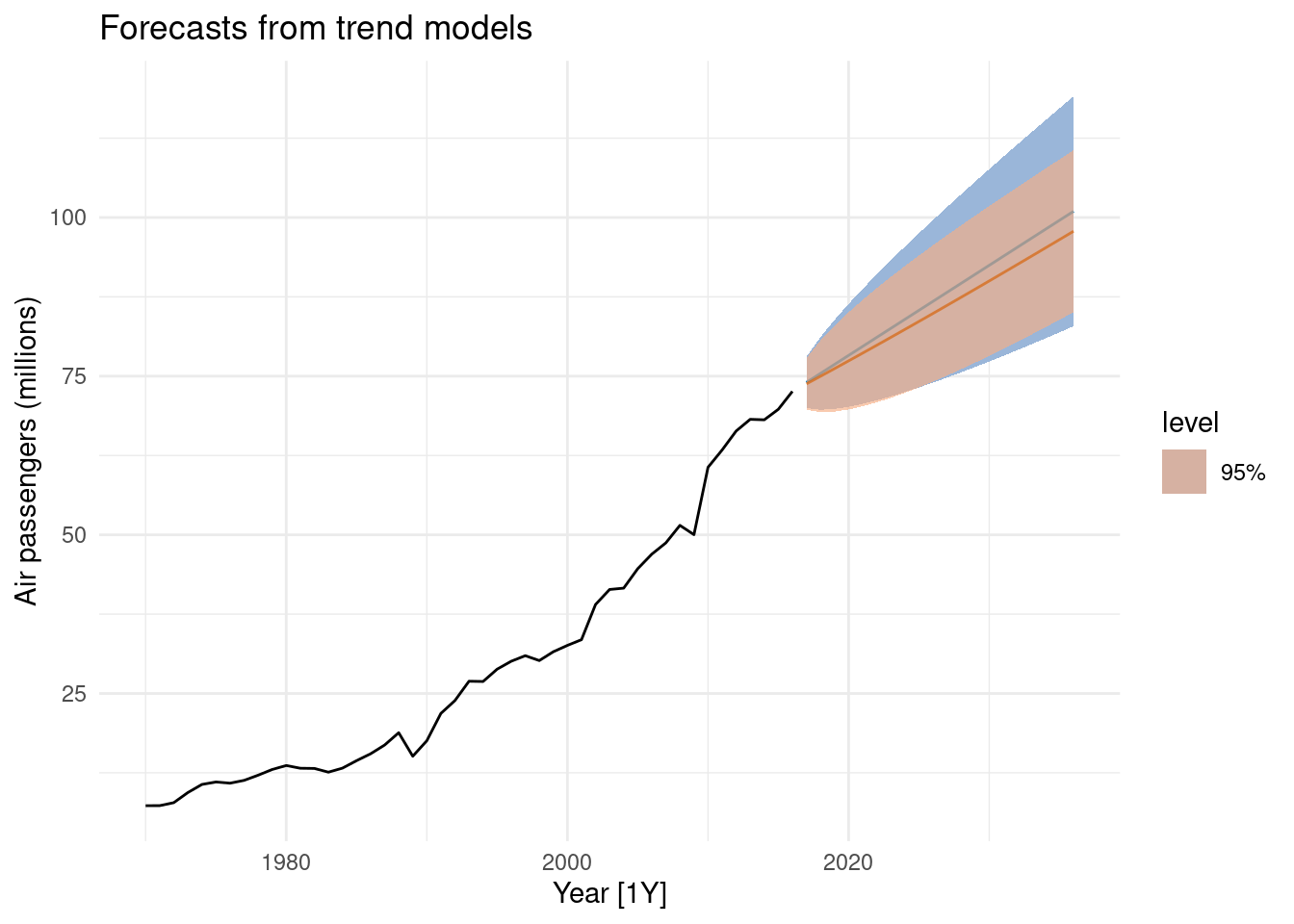

10.5 Difference between Stochastic and deterministic trends

\[y_t=\beta_0+\beta_1x+\eta_t\]

- Deterministic \(\eta_t \sim ARIMA(p,0,q)\)

- Stochastic \(\eta_t \sim ARIMA(p,1,q)\)

fit_deterministic <- aus_airpassengers |>

model(deterministic = ARIMA(Passengers ~ 1 + trend() +

pdq(d = 0)))

fit_stochastic <- aus_airpassengers |>

model(stochastic = ARIMA(Passengers ~ pdq(d = 1)))## Scale for fill_ramp is already present.

## Adding another scale for fill_ramp, which will replace the existing scale.