Correlation

## corrplot 0.90 loaded

library(dplyr, quietly = TRUE)

##

## Attaching package: 'dplyr'

## The following objects are masked from 'package:stats':

##

## filter, lag

## The following objects are masked from 'package:base':

##

## intersect, setdiff, setequal, union

sp500_px <- read.csv("data/sp500_data.csv.gz") %>%

as_tibble()

sp500_sym <- read.csv("data/sp500_sectors.csv", stringsAsFactors = FALSE) %>%

as_tibble()

etfs <- sp500_px %>%

filter(X > "2012-07-01") %>%

select(

any_of(

sp500_sym %>%

filter(sector == "etf") %>%

pull(symbol)

)

)

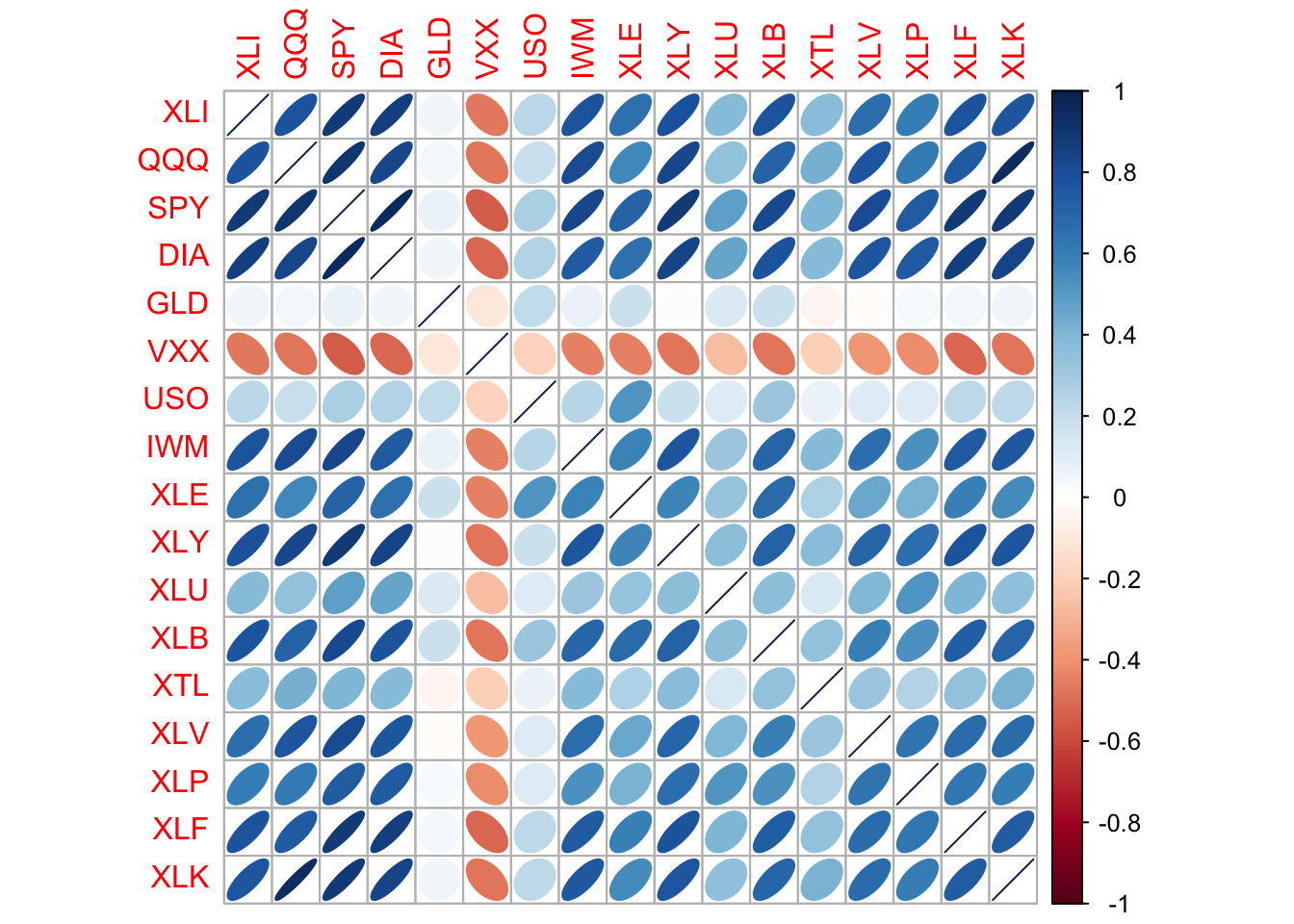

corrplot(cor(etfs), method = "ellipse")